Is The US Economy Headed For a Recession

The short answer is, yes. At some point in the future, the U.S. economy will experience another recession. Our economy has a long history of expansions and retractions. If the answer to the question is so obvious and recessions are a standard component of any economy, why is there so much attention on a looming recession? Because the discussion draws an audience and those in the business want to get your attention. The talking heads and prognostics like to impress with a large serving of historical data, useful in conversation and interesting to some; but I want to know exactly when the recession will begin, how long it will last and the depth of the economic retraction. Answers to these, I'll never have. It's easy to look back and see where we've been, much more difficult (likely impossible) to predict, in a meaningful way, where we are headed. Some investors, even professional money managers may choose to act based on predictions and speculation but I have yet to see the long term benefit of such activity. Being even slightly wrong in the timing could be costly.

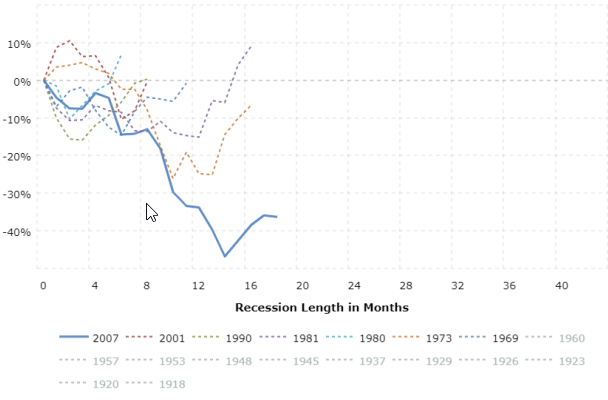

1Macrotrends 100 Year Chart by Recession 1

Is it necessary for stock investors to avoid a recession?

In the past 50 years, The U.S. economy encountered seven recessions lasting in length from 6 to 18 months . The 2007-2009 recession was the longest and most 2 impactful on stock prices. By the end of the year-and-a-half long economic retraction, a broad U.S. stock market index was down approximately 36%. Consider this 3 however, a broad U.S. Stock Market Index delivered an average annualized return of around 10% between January 1, 2003 through December 31, 2013 . The significance of this ten year period is the most impactful recession of the 4 past fifty years occurred in the middle of it. The performance data shared here included the eighteen month recession, it was not void of it.

The 2007 recession officially ended in March 2009. Since then, the average annualized return of a broad U.S. Stock Market Index has been approximately 13% . If we 5 were to base our stock return expectations on the long term average annualized return of 9.80% (from 1926-2018) , we would need to assume a decline in stock prices 6 at some point would be probable in order to revert to the mean. Timing of the reversion, of course, is unknown.

In summary, recessions are part of every economy. Some will be tempted to modify investment holdings to avoid heavy stock allocations during recessionary periods, often with errors in timing (either on the sell side, buy side or both). The inability to time buying and selling with precision could result in lower performance as compared to an investor who maintains their position. While it appears easy to identify "warning signs" when researching past events, it is important to note that complexities in large scale, multifaceted economies can lead to differing outcomes when similar events reoccur. There has been a lot of discussion of late about the inversion of yields between the two year and ten year treasury notes. Some are determined to conclude that since recessions have followed this event on more than one occasion, it has become a reliable indicator of a pending recession. I would caution anyone who may draw such a conclusion while at the same time pointing out several past recessions have not been prefaced by this particular event. In other words, the odds of a recession in the next year or two are likely the same, with or without the recent brief yield curve inversion.