Temporary Decline vs. Permanent Loss

There is debate happening among those with a platform and an opinion over whether or not the U.S. is currently in a recession. If we need to be told we are in a recession, what value is there in knowing? Would you be surprised if I told you an individuals perception of recession status tracks highly with their political party? The party in power (White house and congress) typically has a more positive outlook. This alone should be a red herring to recession reporting. The National Bureau of Economic Research (NBER) published an article that defines a recession as a period of decline in total output, income, employment and trade, usually lasting six months to a year and marked by widespread contractions in many sectors of the economy1. The dictionary has a slightly different definition, a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters. Rather than debate the status of a recession, I believe time is better spent on the likely impact of a potential recession and what, if any, proactive measures should be taken by individual investors. I find analogies work well in these situations. Let's say a car is driving down the interstate at 80 mph in a 65 mph zone. Traffic has picked up and the vehicle is moving at an unsafe speed and needs to slow down, the brake is applied to accomplish a safer environment. Like an automobile, the economy can move too fast. Gross Domestic Product (GDP) is a factor of price and production of domestic goods and services, a popular method of measuring economic growth.

There is debate happening among those with a platform and an opinion over whether or not the U.S. is currently in a recession. If we need to be told we are in a recession, what value is there in knowing? Would you be surprised if I told you an individuals perception of recession status tracks highly with their political party? The party in power (White house and congress) typically has a more positive outlook. This alone should be a red herring to recession reporting. The National Bureau of Economic Research (NBER) published an article that defines a recession as a period of decline in total output, income, employment and trade, usually lasting six months to a year and marked by widespread contractions in many sectors of the economy1. The dictionary has a slightly different definition, a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters. Rather than debate the status of a recession, I believe time is better spent on the likely impact of a potential recession and what, if any, proactive measures should be taken by individual investors. I find analogies work well in these situations. Let's say a car is driving down the interstate at 80 mph in a 65 mph zone. Traffic has picked up and the vehicle is moving at an unsafe speed and needs to slow down, the brake is applied to accomplish a safer environment. Like an automobile, the economy can move too fast. Gross Domestic Product (GDP) is a factor of price and production of domestic goods and services, a popular method of measuring economic growth.

U.S. Real GDP broke $20 trillion at the end of 2021 and the Federal Reserve began a series of rate hikes in March 2022, an action that can be compared to applying the brakes on the economy. The first two quarters of 2022 have reported GDP of approximately $19.90 trillion2 each. Although the intended result, some definitions categorize the slowdown as a recession. Many businesses are short staffed, unemployment remains low, labor force participation rate is at or near historically low levels, products and services are in high demand, corporate profits are stable and overall inflation is still high. It seems contradictory to apply the brakes on GDP for economic health while at the same time labelling the resulting slowdown a recession. Here is a question nobody seems to be asking; if the high prices for goods and services are bad for consumers and producers, how can it also be bad when these prices start to decline? Remember the technical definition of a recession, generally identified by a fall in GDP in two consecutive quarters. Could the technical definition of a recession lead to a more stable, healthier economy? The rhetoric driving fear and negativity is misleading, possibly intentionally. At the end of the day, what actionable information do we have from all of this? Listening to the radio a few days ago I heard an "industry expert" predict the likelihood of a recession in the near future at 60%. What does that even mean and what are we supposed to do with the information? Sell the investments that are the engine to a long term financial plan? Lose sleep at night worrying? Repeat it to friends and family so they can worry too? Often we find the life immediately in front of us differs greatly from the world beyond us. Our ears can find more reasons to worry than our eyes.

My investments are losing value, shouldn't we be doing something about it?

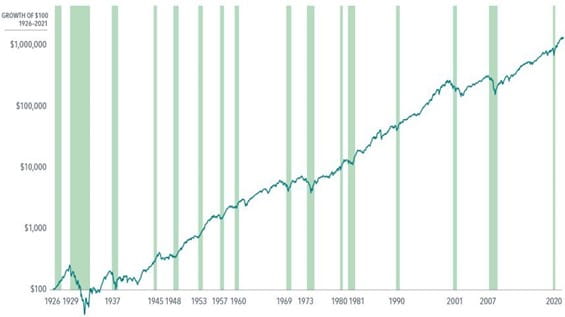

It's never a fun experience when our investments decline in value. It's normal to want to react in a way to prevent further decline. To believe that something needs to be changed is to believe that something went wrong, outside the norm, unexpected. When it comes to capital market investing, history has taught us time and again that price declines are normal and should be anticipated. Yes, even large and uncomfortable declines. From January 1926 through 2021, the broad U.S. Stock market delivered an average annualized return of 10.20%3. If you want data that's more recent, how about 10.90% from 1990 through 2021 or 15.10% from 2010 through 2021. Each of these time periods delivered what I consider a premium rate of return and the best part, selling to avoid further decline was never required. The performance data above includes all past periodic and temporary declines. It was not necessary to make changes when price declines became uncomfortable. In fact, attempts to participate in price increases and avoid price declines (market timing) could, and often does, result in permanent losses never to be recovered. Think of it this way, to benefit from selling when prices are down, one would need to repurchase those same shares when prices are below the sell price. I know from experience the news doesn't turn positive until stock prices are well into recovery, which means it is too late at this point to benefit from the sell decision. One would need to reinvest when the news is worse than when sold. For these reasons, we have no intention to advise you it's time to sell prior to the end of your plan. We are not the individuals talking on radio or television, we are in the trenches with you. The philosophical driven advice that comes from our team is rooted in experience.

Recoveries Can Be Very Strong

The National Bureau of Economic Research (NBER) has recognized twelve recessions since World War II. The chart below shows performance of a broad U.S. stock market index4 six months leading up to the recession, during the recession and 1, 3, 5, and 10 years following the recession. It's noteworthy that half of the returns are positive prior to the recession and half of the returns are positive during the recession. The best news is detailed in what has followed the recession, strong recoveries. The danger in selling prior to, or during a recession is missing the returns that have historically followed some of the worst of times. Ninety-two percent (11/12) of the recognized recessions delivered a positive return one year beyond the end of the recession and 100% of the returns were positive in three, five and ten year periods. This chart illustrates that some of the best performing years have historically followed some of the worst. When you listen to reports about recessions and the stock market, are you hearing about this data? Probably not. As an investor, does this data change the way you feel about your investments? Hopefully so. When we are in consultation with clients who are concerned about declining values and asking if we should be making a change or moving to cash, our answer is a firm no. It's not because we have information nobody else has access to, it's because we have information that others aren't providing.

Market Prices Tend to Recover Ahead of Recessions

The U.S. has recognized 16 recessions since 1926. The broad U.S. stock market index5 has either remained positive or turned positive prior to the end of the recession in 14 of these 16 periods (see chart below). This reaffirms the notion that stock prices are a leading economic indicator and another reason to avoid selling on bad news and buying on good news. Consumer confidence tends to build as news reports shift from negative to positive. In most cases, it's too late to participate fully in stock price recovery. "Big return days are hard to predict, and you really don't want to miss them. If you invested $1,000 in the S&P 500 continuously from the beginning of 1990 through the end of 2020, you would have $20,451. If you missed the single best day, you’d only have $18,329—and only $12,917 if you missed the best five days"6. I believe the most consistent way to capture stock market premiums is to remain fully invested through the end of your plan. Any deviation from that could jeopardize long term performance and the plan's viability. Investors who sell out of fear of further decline may feel good immediately following, but that feeling of "being right" may be temporary and fleeting as market prices recover. One lesson history has taught is 100% of past declines have been temporary. To sell prior to the end of the plan may result in locking in losses that will never be recovered.

Conclusion

It's my fervent belief that the capital markets (stocks and bonds) are intricately woven into the fabric of our economy. Any separation could cause either to falter and cause irreparable damage. This belief is engrained into the investment and planning philosophy of O'Dell Capital Management. It is a result of nearly 32 years of experience, working side by side with individual investors. The advice we share and the philosophies adhered to are driven by a desire to meet prudently established financial goals. To this end, we will not be deterred by economic forecasts or predictions, shifting political winds, high inflation, high taxes or the threat of a recession. None of these have shown to be a long term threat to the resilience and persistence of capital market determination and ingenuity. Any dissenting conclusion would likely have to rely on the old saying "yes, but this time is different". My reply, this time is always different!

1 NBER: Recession or Depression? Reprinted from Across the Board, the Conference Board Magazine (May 1982)

2 YCharts: U.S. Real GDP https://ycharts.com/indicators/us_real_gdp

3 Matrix Book 2022, page 12. CRSP 1-10 Index 1926-2021

4S&P 500 Index

5S&P 500 Index

6Three Crucial Lessons for Weathering the Stock Market’s Storm By Marlena Lee, PhD Global Head of Investment Solutions, DFA