Lets Talk Banks

The banking industry was, once again, brought to the forefront of economic forums on March 10 when the Federal Reserve stepped in and shut down Silicon Valley Bank (SVB). The action was taken to prevent additional depositor requests for funds (sometimes referred to as "a run on the bank") and allow time to determine if SVB is solvent or a possible buyout candidate for another bank. Two weeks later, on March 26, the FDIC announced a purchase and assumption agreement for all deposits and loans of SVB by First Citizen Bank and Trust Company of North Carolina. The deal provided First Citizen Bank the opportunity to purchase a large percentage of SVB's assets, at a discount, while the FDIC holds the remaining securities and assets in receivership. To ease concerns and prevent panic of depositors across the country, the Federal Reserve announced (shortly after closing the doors at SVB) that 100% of all deposits would be protected and available in a matter of days, even though the FDIC Insurance caps at $250,000 per each account ownership category. This action is very telling and indicative of regulatory changes in the future.

According to the FDIC, there have been 563 bank failures from 2001 through 2023. The majority for these, 440, took place from 2009-20121. Why does the failure of SVB garner national attention while hundreds of others have gone mostly unreported? The amount of deposits? Location? Notoriety of depositors? It could be a combination of many things that draw attention to this particular bank.

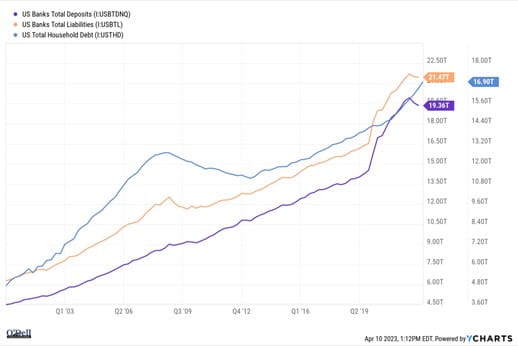

There are several lessons to be learned from past bank failures. First, the Federal Reserve has acted to protect depositors at all costs, regardless of FDIC insurance limits. The system would collapse if faced with widespread and mass requests of funds by depositors. As of December 2022, the deposits in U.S. banks totaled $19.36 trillion. At the same time, U.S. total household debt was nearly $16.90 trillion and U.S. bank's total liabilities reached $21.47 trillion. Clearly, the banking system would be stressed by a large demand for cash by depositors. The Federal Reserve must react in ways to keep confidence high and withdrawal requests low. Second,

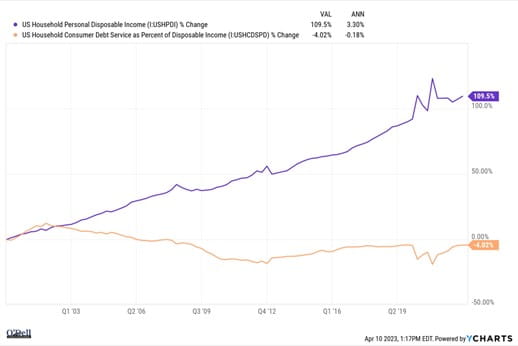

the latest blemish on the banking system is likely to lead to additional regulations and greater enforcement of current regulations. Banks serve a much needed purpose, to provide consumer loans and a safe place for depositing funds. The money used to make these loans comes from depositors, who have zero risk expectations. It can't be overstated how important it is, therefore, for banks to be prudent when lending money. I believe most banks are and the exception to the rule is putting the institution as a whole at risk. Lastly, U.S. household consumer debt as a percentage of disposable income has been trending lower for the past two decades, while disposable income has been climbing. These are positive trends that receive almost no attention. It has been said that it takes ten good news stories to offset one bad. Who knows what the real number is but I certainly believe we, as humans, process the two very differently. Having access to a large quantity of financial related date, I have always found plenty of positive trends even in the midst of overwhelmingly negative headlines.

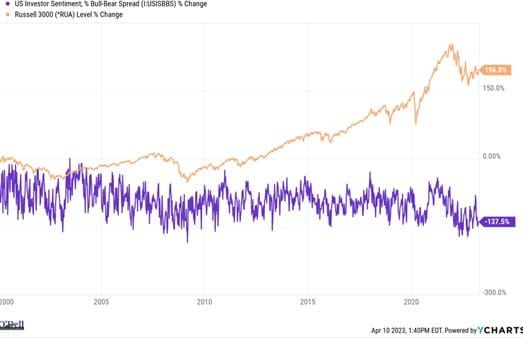

A large part of my job over the past three decades has been to stay informed. Yes, I read plenty of the same headlines as the general public but I also make significant investments in technology that provides access to data most people don't see. I often find the data doesn't correlate with what is being reported. Based on historical averages, 2021 was a good year for the broad U.S. stock market (in terms of performance) and 2022 was bad. Heading into 2023, headlines were overwhelmingly pessimistic. The general consensus among experts was (and remains) a recession was all but imminent. The message, recessions are bad for stocks and investors should be wary. Like so many times in the past, this advice hasn't aged well. Sure, there is plenty of time left in the year and nobody knows how it ill end, but with a year-to-date return of 6.73% 2 for the broad U.S. stock market index3 as of March 31, the year is off to a great start. I have stated many times in the past, uncertainty is a key ingredient in premium returns. The chart below illustrates investor sentiment from 2000-2023 (through March) along with the performance of a broad U.S. stock market index. Following the lead of bearish sentiment could be costly over long periods of time. While sentiment trended lower these past two decades, the index increased 196.8%.

Throughout my career, it has been my observation that most news is not actionable as it relates to investment portfolios. In other words, it can be good for stirring up emotions but as far as providing any information that could be used to improve performance, reduce risk or protect the long term integrity of a financial plan; it simply doesn't deliver. Stay focused on your long term objectives and don't be unduly influenced by today's breaking news, political calamity or water cooler experts.

1 https://www.fdic.gov/bank/historical/bank/

2 YCharts 2023

3 Russell 3000 Index